Mortgage rates 2026 just hit 5.9% — but the housing market data reveals a massive trap for home buyers. Should you buy a house in 2026? Here’s what the real estate numbers actually show. 🏚️

Everyone was waiting for the “magic number.” Rates crossed 6% and buyers were supposed to flood back into the market. So why are 81% of sidelined buyers still sitting on the sidelines? The math tells a brutal story — and most people aren’t seeing it. 💰

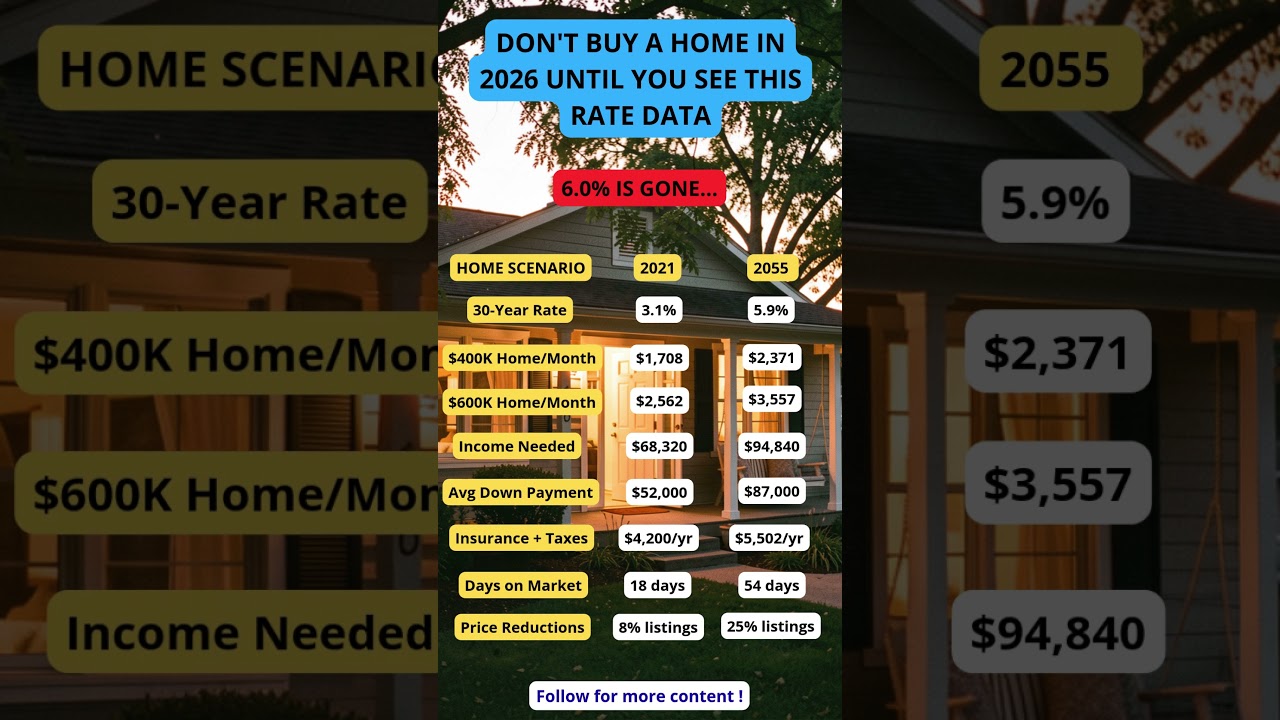

📊 Why the 5.9% mortgage rate is misleading:

Home prices are 42% higher than 2021 — the rate drop saves $472/month but prices erased all gains

A 2021 buyer at 3.1% still pays $663/month LESS than a 2026 buyer at 5.9% on the same home

Inventory is up 8% yet prices are at 0% growth — sellers won’t drop, buyers won’t jump

The average down payment now requires $87,000 cash — blocking most first-time buyers

Insurance and property taxes are up 31% since 2020 — hidden costs nobody talks about

🧠 The psychology trap explained:

In 2024, 67% of buyers said they’d pull the trigger when rates hit 6%. When it happened? Only 19% actually bought. The reason is simple — they were waiting for rates to fix affordability, but rates were never the only problem. Prices never corrected. The true break-even rate where 2026 buying matches 2021 affordability is 4.5% — and that’s not expected until 2028 at the earliest.

✅ What smart buyers should do now:

✅ Run the total cost calculation — rate + price + insurance + taxes combined

✅ Watch inventory trends in YOUR local market — national data hides local opportunities

✅ Negotiate hard — 1 in 4 listings already cut prices, more sellers are softening

✅ Don’t buy based on rates alone — buy when the total monthly payment fits your life

✅ If renting costs less than owning in your market — renting is the smarter play in 2026

💬 Are you waiting to buy a home? What rate would actually make you pull the trigger?

📍 Sources: Freddie Mac March 2026, NAR Q1 Report, Zillow Market Pulse, Redfin Buyer Survey, Bank of America Forecast 2026

Everyone was waiting for the “magic number.” Rates crossed 6% and buyers were supposed to flood back into the market. So why are 81% of sidelined buyers still sitting on the sidelines? The math tells a brutal story — and most people aren’t seeing it. 💰

📊 Why the 5.9% mortgage rate is misleading:

Home prices are 42% higher than 2021 — the rate drop saves $472/month but prices erased all gains

A 2021 buyer at 3.1% still pays $663/month LESS than a 2026 buyer at 5.9% on the same home

Inventory is up 8% yet prices are at 0% growth — sellers won’t drop, buyers won’t jump

The average down payment now requires $87,000 cash — blocking most first-time buyers

Insurance and property taxes are up 31% since 2020 — hidden costs nobody talks about

🧠 The psychology trap explained:

In 2024, 67% of buyers said they’d pull the trigger when rates hit 6%. When it happened? Only 19% actually bought. The reason is simple — they were waiting for rates to fix affordability, but rates were never the only problem. Prices never corrected. The true break-even rate where 2026 buying matches 2021 affordability is 4.5% — and that’s not expected until 2028 at the earliest.

✅ What smart buyers should do now:

✅ Run the total cost calculation — rate + price + insurance + taxes combined

✅ Watch inventory trends in YOUR local market — national data hides local opportunities

✅ Negotiate hard — 1 in 4 listings already cut prices, more sellers are softening

✅ Don’t buy based on rates alone — buy when the total monthly payment fits your life

✅ If renting costs less than owning in your market — renting is the smarter play in 2026

💬 Are you waiting to buy a home? What rate would actually make you pull the trigger?

📍 Sources: Freddie Mac March 2026, NAR Q1 Report, Zillow Market Pulse, Redfin Buyer Survey, Bank of America Forecast 2026